5 Ways Debt or Bad Credit May Affect Your Employment

Most Americans know that a high debt load and ongoing credit problems could prevent them from being approved for new credit. But did you know that it could also jeopardize your employment potential?

Most Americans know that a high debt load and ongoing credit problems could prevent them from being approved for new credit. But did you know that it could also jeopardize your employment potential?

If the idea of your debt impacting your job — or future promotions — is new, here are five reasons that employers could be wary of those with a worrisome credit history.

1. You May Experience More Temptation to Steal

Any American suffering from a financial emergency — whether it be job loss, expensive medical treatment, a divorce, or other challenges — must decide how to handle the increasing pressure. Many turn to sources of money and credit in order to keep going. And while some willingly turn to legal tools like bankruptcy, that can be a hard call for many others.

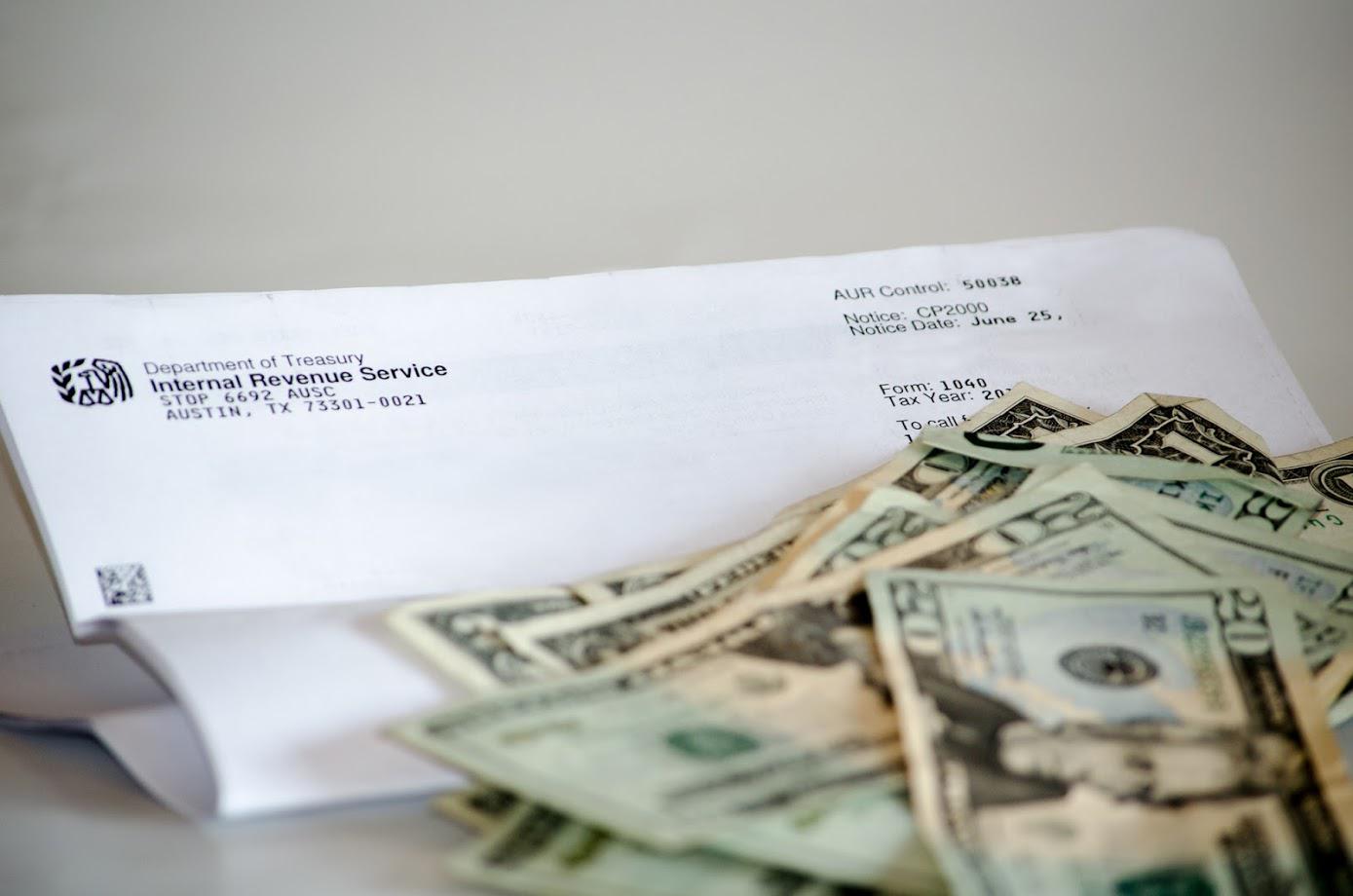

Any American suffering from a financial emergency — whether it be job loss, expensive medical treatment, a divorce, or other challenges — must decide how to handle the increasing pressure. Many turn to sources of money and credit in order to keep going. And while some willingly turn to legal tools like bankruptcy, that can be a hard call for many others. No one enjoys dealing with the IRS tax collection process, so few people are well-versed in tax collection terminology. But when you find yourself entangled in unpaid tax debts, you need to understand what all the various terms mean and how they affect you. To help you navigate your own debt challenges, here is a short guide to six key terms you’ll encounter along the way.

No one enjoys dealing with the IRS tax collection process, so few people are well-versed in tax collection terminology. But when you find yourself entangled in unpaid tax debts, you need to understand what all the various terms mean and how they affect you. To help you navigate your own debt challenges, here is a short guide to six key terms you’ll encounter along the way.